The 5 Crucial Differences Between Secured and Unsecured Credit Cards: Which is Right for You?

Related Articles: The 5 Crucial Differences Between Secured and Unsecured Credit Cards: Which is Right for You?

- Tricks of Credit Card Company

- 5 Unbelievable Credit Card Benefits That Can Transform Your Finances

- 5 Crucial Steps To Unlocking Your Financial Freedom With A Bad Credit Card

- The 5-Step Credit Card Application Process: A Comprehensive Guide To Financial Freedom

- Credit card Examinations – Picking The Best Arrangement

Introduction

In this auspicious occasion, we are delighted to delve into the intriguing topic related to The 5 Crucial Differences Between Secured and Unsecured Credit Cards: Which is Right for You?. Let’s weave interesting information and offer fresh perspectives to the readers.

The 5 Crucial Differences Between Secured and Unsecured Credit Cards: Which is Right for You?

The world of credit cards can seem confusing, especially when you’re just starting out. Two common terms you’ll encounter are "secured" and "unsecured" credit cards. While both can be valuable tools for building credit and managing your finances, they have key differences that can significantly impact your journey towards financial freedom. This article will delve into the 5 crucial distinctions between these two types of cards, helping you make an informed decision about which one is right for you.

Understanding Secured Credit Cards

Imagine a credit card with training wheels. That’s essentially what a secured credit card is. It’s a great option for individuals with limited or no credit history, as it provides a safety net for both you and the issuer.

Here’s how it works:

- Security Deposit: You’ll need to make a security deposit, usually in the form of cash or a savings account, which acts as collateral. This deposit, often equivalent to your credit limit, ensures the issuer is covered if you default on your payments.

- Lower Credit Limits: Secured cards generally have lower credit limits compared to unsecured cards, reflecting the lower risk associated with them.

- Building Credit: The primary benefit is that responsible use of a secured card helps you establish credit history. Your payment behavior is reported to credit bureaus, allowing you to build a positive credit score over time.

- Potential for Gradual Upgrade: Many issuers offer the option to upgrade to an unsecured card once you demonstrate responsible credit management. This transition often occurs after a set period of time, usually 6-12 months, and requires a good payment history.

Understanding Unsecured Credit Cards

Unsecured credit cards are the "grown-up" version of credit cards. They are issued based on your creditworthiness, and the issuer relies on your ability to repay the balance.

Here’s what sets them apart:

- No Security Deposit: Unlike secured cards, you don’t need to make a security deposit. The issuer trusts you to repay the balance based on your credit history and financial stability.

- Higher Credit Limits: Unsecured cards generally offer higher credit limits, reflecting the issuer’s confidence in your ability to manage the credit responsibly.

- Rewards and Benefits: Unsecured cards often come with attractive perks like rewards programs, travel benefits, and purchase protection.

- Higher Interest Rates: While the potential rewards are greater, unsecured cards usually have higher interest rates compared to secured cards due to the increased risk for the issuer.

5 Crucial Differences to Consider:

Now that you have a basic understanding of secured and unsecured credit cards, let’s delve deeper into the 5 key differences that can help you decide which is best for your situation:

1. Credit History:

- Secured: Ideal for individuals with limited or no credit history. It provides a foundation for building a positive credit score.

- Unsecured: Requires established credit history and a good credit score.

2. Security Deposit:

- Secured: Requires a security deposit, usually equivalent to your credit limit, which serves as collateral.

- Unsecured: No security deposit required.

3. Credit Limit:

- Secured: Typically offers lower credit limits due to the lower risk associated with the card.

- Unsecured: Usually offers higher credit limits, reflecting the issuer’s confidence in your creditworthiness.

4. Interest Rates:

- Secured: Generally have lower interest rates compared to unsecured cards due to the reduced risk for the issuer.

- Unsecured: Usually have higher interest rates reflecting the increased risk for the issuer.

5. Rewards and Benefits:

- Secured: Often offer limited or basic rewards programs.

- Unsecured: Typically offer a wider range of rewards programs, travel benefits, and purchase protection.

Which Type of Card is Right for You?

The choice between a secured and unsecured credit card depends on your individual circumstances and financial goals.

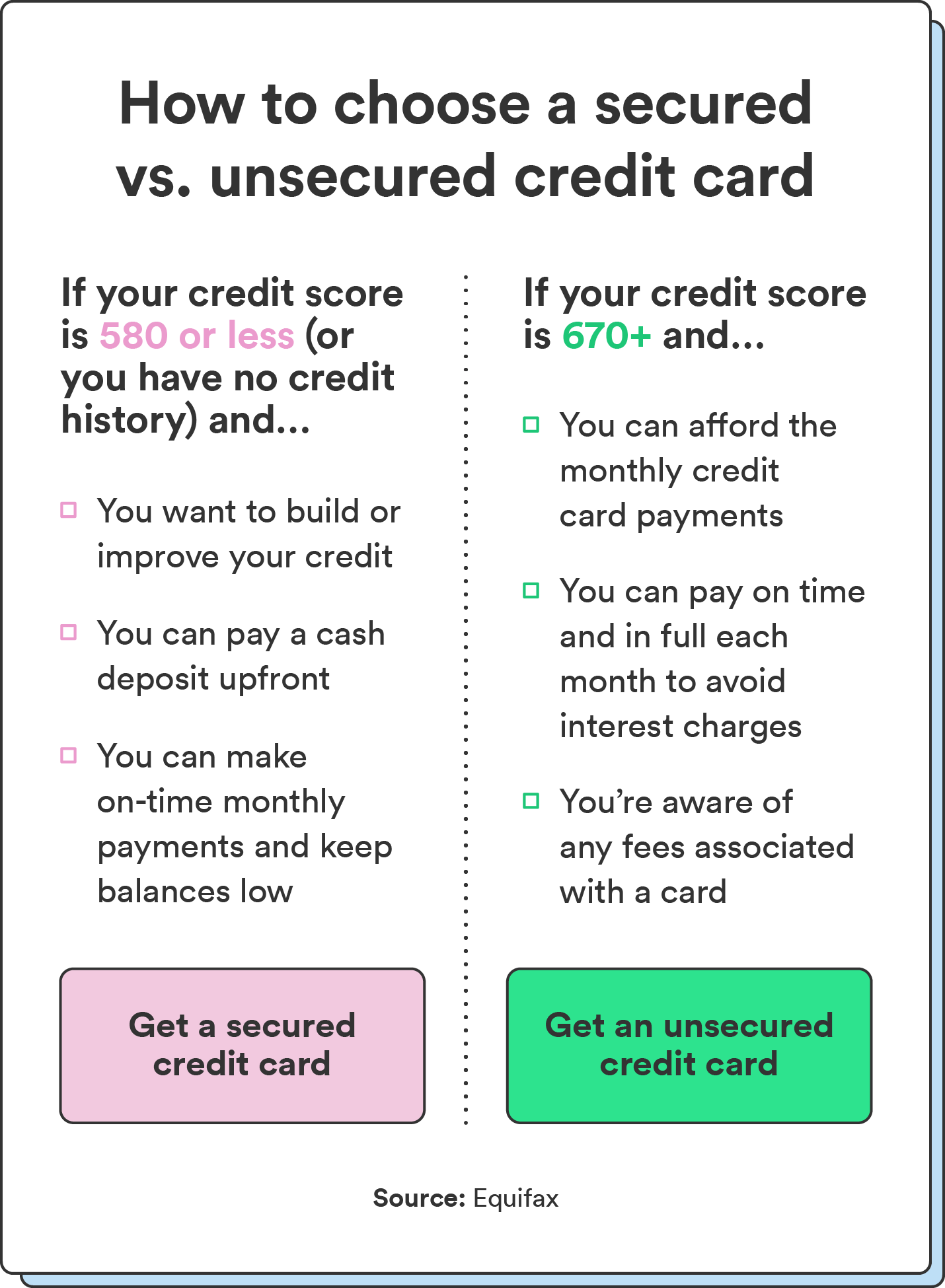

Secured credit cards are a great option if:

- You have limited or no credit history.

- You’re looking to build a positive credit score.

- You want to minimize the risk of overspending.

Unsecured credit cards are a better fit if:

- You have established credit history and a good credit score.

- You need a higher credit limit.

- You’re seeking attractive rewards and benefits.

Building a Solid Credit Foundation:

Whether you opt for a secured or unsecured credit card, building a solid credit foundation is crucial. Here are some tips for responsible credit card use:

- Pay Your Bills on Time: Consistent on-time payments are the cornerstone of a good credit score.

- Keep Your Credit Utilization Low: Aim to keep your credit utilization ratio, which is the amount of credit you’re using compared to your total available credit, below 30%.

- Monitor Your Credit Report: Regularly check your credit report for any errors or discrepancies.

- Limit Applying for New Credit: Too many credit inquiries can negatively impact your credit score.

Conclusion:

Secured and unsecured credit cards both have their own advantages and disadvantages. Understanding the differences between them and carefully considering your financial goals and credit history will enable you to make the right choice for your needs. By utilizing credit cards responsibly, you can build a positive credit score, access valuable financial tools, and pave the way for a brighter financial future. Remember, credit cards are a powerful tool, but like any tool, they must be used responsibly to achieve desired outcomes.

:max_bytes(150000):strip_icc()/secured-vs-unsecured-credit-card-final-89a160834c364a43a0913e67176e0215-f0faefaa72694b7e9ce3e5efd853a502.png)

Closure

Thus, we hope this article has provided valuable insights into The 5 Crucial Differences Between Secured and Unsecured Credit Cards: Which is Right for You?. We hope you find this article informative and beneficial. See you in our next article!

Sponsored Website: paid4link.com

{kind=link}